Germany Anemia Treatment Market Size and Forecast 2026–2034

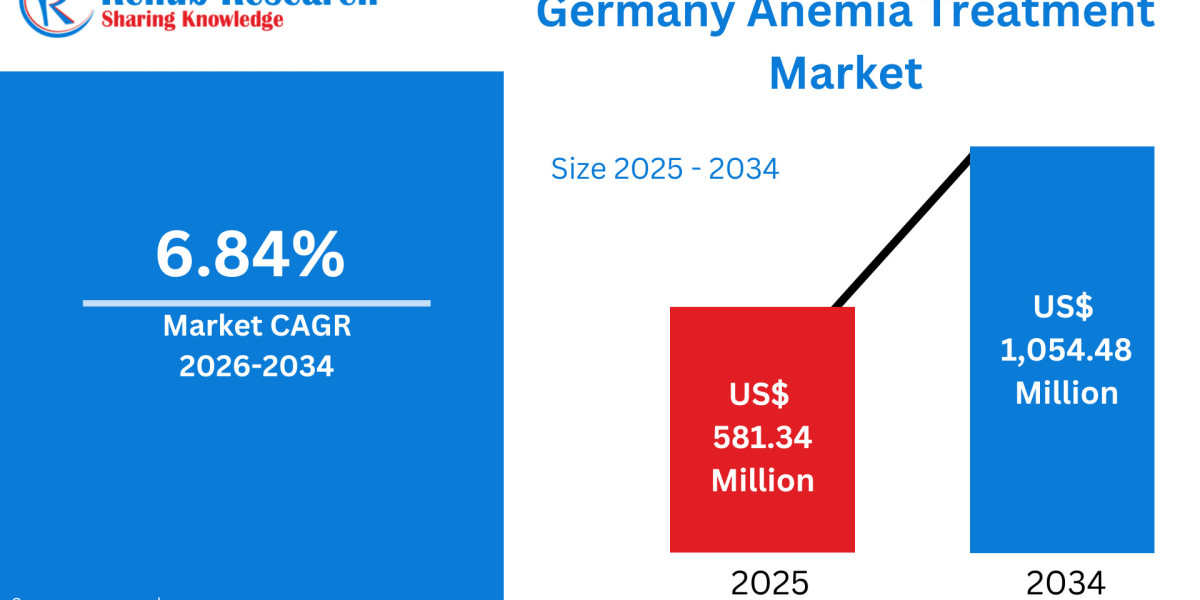

According to Renub Research Germany anemia treatment market is entering a strong growth phase, driven by demographic changes, evolving clinical practices, and sustained healthcare investment. The market is expected to grow from US$ 581.344 million in 2025 to US$ 1,054.48 million by 2034, registering a CAGR of 6.84% from 2026 to 2033. This expansion reflects the increasing burden of iron-deficiency anemia, chronic kidney disease (CKD)–related anemia, oncology-associated anemia, and rare hematological disorders.

Germany’s well-structured healthcare system, comprehensive reimbursement framework, and emphasis on early diagnosis provide fertile ground for market growth. The adoption of advanced intravenous (IV) iron therapies, erythropoiesis-stimulating agents (ESAs), and novel hypoxia-inducible factor prolyl hydroxylase (HIF-PH) inhibitors is reshaping anemia management across hospitals, dialysis centers, and outpatient clinics. As awareness improves and screening programs expand, demand for effective, fast-acting, and patient-friendly anemia treatments continues to rise nationwide.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=germany-anemia-treatment-market-p.php

Germany Anemia Treatment Industry Overview

Anemia treatment in Germany focuses on correcting low hemoglobin levels while addressing the underlying cause of reduced red blood cell production. Iron-deficiency anemia, the most common type, is typically managed with oral iron supplements for mild cases and IV iron for patients who require rapid correction or cannot tolerate oral formulations. Chronic disease–related anemia, especially linked to CKD, cancer, and inflammatory disorders, often requires ESAs alongside iron supplementation. In severe or acute cases, blood transfusion remains an option, though modern guidelines prioritize pharmacological approaches to minimize transfusion dependence.

Germany’s clinical protocols emphasize precision diagnostics, including ferritin, transferrin saturation, and inflammatory markers, ensuring therapy is tailored to the patient’s condition. Nutritional counselling, regular monitoring, and dose optimization are standard components of care. The country’s strong network of nephrology centers, oncology clinics, and university hospitals supports integrated anemia management. These factors collectively enhance treatment outcomes and contribute to the steady expansion of the anemia treatment market.

Key Growth Drivers in the Germany Anemia Treatment Market

Rising Prevalence of Chronic Diseases

The growing incidence of chronic diseases is a primary driver of anemia treatment demand in Germany. CKD, cancer, autoimmune disorders, and gastrointestinal diseases frequently cause or exacerbate anemia. As Germany’s population ages, the prevalence of these conditions increases, leading to sustained demand for anemia therapies. Dialysis patients, in particular, require long-term ESA and IV iron therapy, making CKD anemia a major revenue contributor.

Robust screening protocols and standardized diagnostic pathways ensure anemia is identified early as a comorbidity, rather than treated as a secondary concern. This integration of anemia management into chronic disease care plans significantly boosts treatment volumes and long-term market growth.

Advanced Healthcare Infrastructure and Innovation

Germany’s world-class healthcare infrastructure plays a crucial role in market development. University hospitals and specialized hematology centers employ advanced diagnostic technologies, enabling accurate classification of anemia types. The presence of leading pharmaceutical innovators such as Sanofi, Novartis, Roche, and Bayer ensures continuous R&D investment in iron formulations, biosimilars, and novel agents.

Digital health integration, including electronic medical records and remote monitoring, improves adherence and outcome tracking. Germany’s participation in multinational clinical trials accelerates access to innovative therapies, reinforcing its position as a leading European anemia treatment market.

Strong Reimbursement and Public Health Awareness

Germany’s statutory health insurance system provides broad reimbursement coverage for anemia therapies, including oral iron, IV iron, ESAs, and emerging treatments. Clinical guidelines issued by professional bodies ensure uniform standards of care across regions. Public health initiatives focused on maternal health, elderly care, and workplace wellness promote routine screening, leading to higher diagnosis rates.

These measures reduce financial barriers, encourage early intervention, and support consistent therapy adherence. As awareness of iron deficiency and fatigue-related disorders grows, patient engagement with anemia treatment continues to strengthen.

Challenges in the Germany Anemia Treatment Market

High Cost of Advanced Therapies

Despite comprehensive reimbursement, the high cost of innovative anemia treatments poses challenges. Biologics, long-acting ESAs, and HIF-PH inhibitors place pressure on healthcare budgets, particularly in public hospitals. Cost-effectiveness assessments and regional price negotiations can delay market entry for premium therapies.

Long-term treatment requirements for CKD and oncology patients further increase expenditure, encouraging the use of biosimilars and generics. While cost containment supports system sustainability, it may limit rapid adoption of next-generation therapies.

Diagnosis Gaps and Awareness Limitations

Underdiagnosis remains an issue, especially for mild or asymptomatic anemia. Younger adults, migrant populations, and individuals with limited nutritional awareness may delay seeking care. In rural areas, access to specialist diagnostics can be limited, leading to later-stage detection.

Although public campaigns exist, anemia often receives less attention than other chronic conditions. Addressing these gaps through broader education and proactive screening is essential to unlocking the market’s full potential.

City-Level Insights: Germany Anemia Treatment Market

Frankfurt Anemia Treatment Market

Frankfurt benefits from a dense concentration of hospitals, research institutions, and pharmaceutical companies. Advanced diagnostic capabilities and access to modern therapies support early adoption of IV iron, ESAs, and biologics. Corporate wellness programs and a diverse population further drive screening and preventive care demand.

Munich Anemia Treatment Market

Munich’s market is supported by strong academic medicine and biotechnology activity. Personalized treatment pathways for CKD-related anemia, oncology-associated anemia, and autoimmune disorders are widely implemented. Preventive screening programs and occupational health initiatives enhance market penetration.

Hamburg Anemia Treatment Market

Hamburg’s anemia treatment demand is shaped by its industrial workforce and strong nephrology network. High screening rates for nutritional deficiencies and fatigue-related conditions sustain steady demand for iron therapies and ESAs. Research collaboration with global pharmaceutical firms supports innovation.

Berlin Anemia Treatment Market

Berlin stands out as a research-driven market, supported by leading academic institutions and a vibrant biotech ecosystem. Public health initiatives targeting vulnerable populations and strong outpatient care networks expand access to diagnosis and treatment. Digital health adoption further enhances follow-up and adherence.

Recent Developments in the Germany Anemia Treatment Market

Germany continues to attract pharmaceutical investment and strategic partnerships. In 2024, Sanofi announced a major manufacturing expansion in Frankfurt, strengthening domestic production capacity and long-term supply resilience.

In 2023, Akebia Therapeutics entered a licensing agreement with MEDICE to commercialize vadadustat across Europe, including Germany. This development expands treatment options for CKD-related anemia and highlights growing interest in HIF-PH inhibitors.

Germany Anemia Treatment Market Segmentation Analysis

By Disease Type

Iron-deficiency anemia represents the largest segment due to its high prevalence among women, elderly patients, and individuals with nutritional deficiencies. CKD-related anemia follows closely, driven by the growing dialysis population. Rare disorders such as aplastic anemia, thalassemia, and sickle cell anemia contribute smaller but clinically significant shares.

By Therapy Class

Oral iron supplements dominate in volume, while IV iron therapies account for higher revenue due to premium pricing. ESAs remain essential for chronic disease management, and HIF-PH inhibitors are emerging as a promising alternative. Iron chelators serve niche indications, particularly in transfusion-dependent patients.

By Route of Administration

Oral therapies lead in outpatient settings, while injectable formulations dominate hospitals and dialysis centers. The preference for injectable therapies reflects the need for rapid correction and improved compliance in severe cases.

Competitive Landscape and Key Players

The Germany anemia treatment market is moderately consolidated, with strong participation from multinational and regional pharmaceutical companies. Key players include Pfizer, Takeda, Johnson & Johnson, GSK plc, Vertex Pharmaceuticals, and Biocon Biologics.

Companies compete on product efficacy, safety, pricing, and supply reliability. Strategic partnerships, biosimilar launches, and portfolio diversification are common strategies to strengthen market presence.

Future Outlook for the Germany Anemia Treatment Market

The Germany anemia treatment market is poised for sustained growth through 2034. Demographic aging, rising chronic disease prevalence, and continuous innovation will remain key growth drivers. Expansion of IV iron usage, increased adoption of HIF-PH inhibitors, and broader screening initiatives are expected to reshape treatment patterns.

With strong reimbursement, advanced healthcare infrastructure, and an innovation-friendly environment, Germany will continue to be one of Europe’s most attractive markets for anemia treatment. Companies that balance cost-effectiveness with clinical innovation are best positioned to capitalize on emerging opportunities in this evolving landscape.