Fintech companies, NBFCs, and digital lending platforms in India operate in a high-volume, high-risk environment. Every day, thousands of customers are onboarded digitally for loans, credit lines, and financial products. While speed is critical to stay competitive, compliance and identity accuracy cannot be compromised. This balance is where KYC plays a decisive role.

Among the various identity documents used in India, the Voter ID holds unique importance due to its wide reach and acceptance. Integrating a Voter ID Verification API into KYC workflows helps lending platforms strengthen identity checks, reduce fraud, and expand access to financial services without slowing down onboarding.

The KYC Challenge for Fintechs and Lenders

Digital lending has removed physical barriers, but it has also increased exposure to identity-related risks. Fake profiles, impersonation, and duplicate identities can lead to loan defaults, regulatory issues, and financial losses. Manual verification methods struggle to keep up with the scale and speed required by modern platforms.

Fintechs and NBFCs need KYC solutions that are fast, reliable, and inclusive. Relying only on a limited set of documents can exclude potential customers, especially in semi-urban and rural areas. This is why platforms are adopting additional verification layers to strengthen identity validation.

Why Voter ID Matters in Financial KYC

The Voter ID is one of the most widely held identity documents in India. It covers a broad demographic, including individuals who may not have access to other financial identifiers. This makes it especially valuable for lenders looking to expand responsibly into underbanked segments.

Unlike documents that are used only for specific financial purposes, Voter ID is commonly accepted as proof of identity. When verified digitally, it becomes a strong input for KYC processes, helping platforms confirm identity with greater confidence.

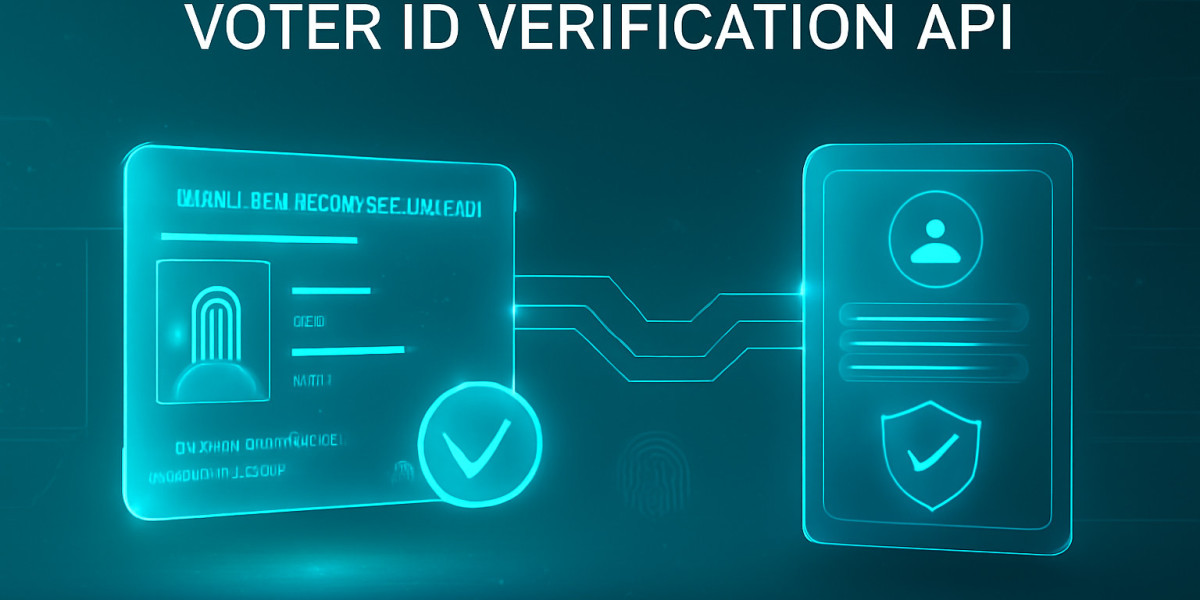

What Is a Voter ID Verification API?

A Voter ID Verification API is a digital service that allows platforms to validate voter identity details against official records. By submitting a Voter ID number, lenders can check whether the ID is valid and whether the associated details match the customer’s information.

Instead of manual document review or offline checks, APIs return structured responses in real time. This makes voter ID verification suitable for automated onboarding flows used by fintechs and lending platforms operating at scale.

How Voter ID API Strengthens KYC for Fintechs and NBFCs

Faster and Smoother Onboarding

Speed is a major differentiator in digital lending. A Voter ID API enables instant identity checks, reducing delays caused by manual verification. Customers can complete KYC quickly, improving conversion rates and user experience.

Reduced Identity Fraud

Fraudsters often exploit gaps in identity verification. Voter ID verification adds an additional layer that makes impersonation and fake profiles harder to execute. Validating identity against trusted records helps prevent risky users from entering the system.

Improved Inclusivity

Many potential borrowers may not have multiple identity documents readily available. Supporting Voter ID verification allows lenders to onboard a wider audience while maintaining compliance standards. This supports financial inclusion without increasing risk.

Consistent KYC Standards

APIs apply the same verification logic across all applications. This consistency reduces human error and ensures that KYC checks are uniform, regardless of onboarding volume or geography.

Key Use Cases Across Lending Workflows

Customer Onboarding

During onboarding, Voter ID verification helps confirm customer identity before loan approval. It acts as an additional validation layer alongside other KYC checks.

Risk Assessment and Profiling

Accurate identity data improves customer profiling and risk assessment. Clean KYC records support better credit decisions and healthier loan portfolios.

Re-KYC and Account Reviews

Customer details may change over time, or regulatory requirements may demand periodic re-verification. Voter ID APIs support efficient re-KYC without requiring physical documents.

Compliance and Audit Support

Maintaining verified identity records helps fintechs and NBFCs demonstrate compliance during audits. Automated verification logs improve transparency and governance.

Benefits of Using Voter ID API for Lending Platforms

One of the biggest benefits is trust. Verified identities reduce uncertainty and strengthen confidence in digital lending operations.

Operational efficiency also improves. Automation lowers manual workload and allows teams to focus on exceptions rather than routine checks.

From a regulatory perspective, voter ID verification supports robust KYC frameworks and helps platforms align with evolving compliance expectations.

Scalability is another key advantage. As onboarding volumes grow, APIs ensure that verification quality remains consistent without increasing operational complexity.

Best Practices for Responsible Implementation

Voter ID verification should be used as part of a layered KYC approach, not as a standalone check. Combining it with other identity and risk signals creates a stronger verification framework.

Data security is critical. Identity information must be protected through encryption, controlled access, and minimal data retention. Transparency with customers about how their data is used also helps build long-term trust.

Clear internal policies should define how voter ID API impacts approval decisions to ensure fairness and consistency.

Conclusion

For fintechs, NBFCs, and lending platforms, strong KYC is the foundation of sustainable growth. As digital onboarding scales across India, relying on limited or manual verification methods increases risk and slows down operations.

A Voter ID Verification API helps lenders strengthen identity checks, reduce fraud, and expand access to financial services responsibly. By combining speed, inclusivity, and compliance, voter ID-based verification has become an important component of modern KYC strategies in India’s evolving digital lending ecosystem.